Yet another airline has collapsed – this time British operation Flybmi, costing almost 400 jobs as hundreds of flights were cancelled at short notice.

It is the latest in a string of recent European airline failures, including Air Berlin, Alitalia, Monarch, Primera, Azur and Cobalt. This is despite years of good growth in worldwide air passenger demand, including in Europe. So why are so many airlines going out of business?

Aviation is an unattractive industry from an investor point of view at the best of times, notwithstanding the passenger growth. Aeroplanes are expensive assets with few alternative uses, which limits the ability of airlines to reduce their capacity during lean periods – compared to, say, a manufacturing business that can close a plant and lay off workers.

Airlines also have to deal with fluctuating expenses like fuel, which accounts for around a third of total costs. There is also extensive regulation, combative unions, relatively low barriers to entry and the fact that travellers can so easily shop around.

The sector did become more profitable in the early years of this decade, but this was due to lower fuel prices rather than any underlying improvements.

When fuel prices began climbing again in 2016, airlines were hit. This is particularly true of those like Flybmi and Monarch which were buying fuel in pounds sterling, since the currency has weakened in the wake of the 2016 Brexit vote. The political uncertainty has not helped British airlines either – though equally we must generally beware of companies using this as a scapegoat for bad performance.

The net result is that it is very difficult for airlines to consistently turn a profit. Business failings are particularly likely to be punished – in the case of Flybmi, for instance, neither the company’s costs nor its fares were low enough to compete effectively. It didn’t have enough passengers for the number of routes it was offering, and could not change capacity without incurring more costs.

It seems extremely likely that there will be more collapses in the sector, and more consolidation as weaker players get weeded out – Ryanair’s takeover of the Austrian airline Laudamotion is one recent example; another is the Virgin Atlantic tie-up with Flybe.

The attractions of growing through acquisition are much the same as in many sectors: it gives you greater control of purchasing costs by boosting your negotiating power, while also potentially reducing the downward pressure on ticket prices by taking competitors out of the market.

Takeovers are not a panacea, however, since fuel prices will still fluctuate and underlying negatives like high sunk costs into aeroplanes don’t go away. At the same time, there is no shortage of competition from new entrants who are seemingly oblivious to the challenges in the industry.

Related course: Executive MBA

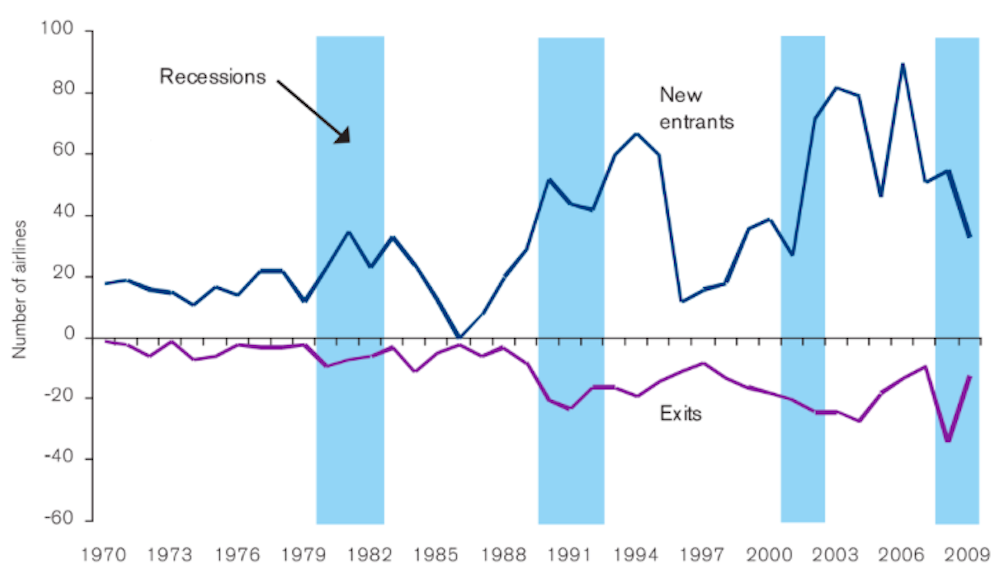

In 2017, for example, 79 new airlines launched around the world at the same time as 25 went bust. In Europe, it was 29 entrants and 14 collapses. This rate of market entry is surely unsustainable, particularly in a mature market.

It’s also financially irrational when you reflect that the airlines sector produces among the poorest returns on investment. Yet even during recessions, the rate of airline launches sometimes increases – see the graphic below.

Your chances of launching a successful airline nowadays are far lower than, say, in the 1970s, when far fewer went under: there is overcapacity across the industry now, with one in five passenger seats empty across the world. Today’s competition rules also make it much harder for nations to prop up failed airlines.

The trouble is that this is a sexy industry; who wants to make widgets when you can pose in front of a plane? There is also a lot of hubris – driven by the handful of airlines that do make good returns, even as most do not.

This brings me to Ryanair, the biggest carrier in Europe, which has itself issued several profit warnings – the most recent in January. The Irish airline, which boasts a 15 per cent market share and 142 million passengers, blamed the warning on reduced ticket prices in response to cut-throat competition.

But don’t look to Ryanair to become another of the casualties: chief executive Michael O'Leary still expects the company to make profits after tax of around €1 billion to €1.1 billion (£871 million to £958 million) for the financial year 2019.

Ryanair is in line to make a net profit margin in the region of the 20 per cent it has achieved in recent years, higher than any European competitor.

As the airline with the highest internal efficiency by some distance, the lowest customer fares, an ambitious expansion plan and the greatest geographical coverage in Europe, Ryanair retains its fundamental competitive advantages.

Softer fares might have hurt the company, but they will have hurt other European airlines much more. Besides all the other factors that make life so difficult for the likes of Flybmi, getting thumped by Ryanair is another almost inevitable pitfall of being in the airline business.

This article is republished from The Conversation. Read the original article.

Loizos Heracleous is Professor of Strategy and teaches Strategic Management on the Doctorate in Business Administration plus Strategy and Practice on the Executive MBA and Executive MBA (London).

Follow Loizos Heracleous on Twitter @Strategizing.

For more articles like this download Core magazine here.

X

X Facebook

Facebook LinkedIn

LinkedIn YouTube

YouTube Instagram

Instagram Tiktok

Tiktok